Choosing between a new car vs used car is one of the first big decisions you will face as a first-time buyer. It often feels confusing because both options seem right in different ways. You might want the reliability and peace of mind that comes with a new car, but at the same time, the lower price of a used car can feel like the smarter financial choice.

This decision matters more than it seems. It affects how much you spend upfront, how stable your ownership experience will be, and how much your car will cost you over time. A new car usually means higher payments and quicker loss in value, but fewer unexpected problems. A used car can save you money at the start, but it may come with unknown history and possible repair costs later.

In this guide, you will learn the key differences, real cost factors, depreciation impact, and practical trade-offs. This helps you make a more confident decision as you move forward with how to buy a car for the first time.

The main difference in a new car vs used car choice is that new cars offer more reliability, full warranty coverage, and fewer early problems, while used cars are more affordable and lose value more slowly but can come with condition and maintenance risks. This difference between the two directly affects how much you pay upfront, how reliable the car will be, and how likely you are to face unexpected costs.

For a first-time buyer, this comes down to higher upfront cost with peace of mind, or lower cost with some uncertainty.

New Car vs Used Car: Key Differences First-Time Buyers Should Know

The key differences between a new and used car come down to cost, reliability, and long-term value. Understanding these differences helps you see what you are paying for and what kind of ownership experience you can expect. This makes it easier to compare both options before looking at the details.

Quick Comparison: New vs Used Car at a Glance

| Factor | New Car | Used Car |

| Price | Higher | Lower |

| Depreciation | Fast | Slower |

| Reliability | High | Varies |

| Maintenance | Predictable | Variable |

| Features | Latest | Older |

| Insurance | Higher | Lower |

What Defines a New Car

A new car is a vehicle that has never been owned or registered before. It usually comes from the latest model year and includes full manufacturer warranty coverage, especially on crucial safety features like ABS, electronic stability control, traction control, automatic emergency braking, airbags etc.

Because it has no prior usage, there is no wear and tear. This makes ownership more stable in the first few years. You are less likely to deal with repairs, and most issues, if they occur, are covered under warranty. For a first-time buyer, this reduces stress and makes the experience easier to manage.

What Defines a Used Car

A used car is a vehicle that has had one or more previous owners. Its condition depends on mileage, maintenance history, and how it was driven.

Used cars cost less because they have already gone through early depreciation. This makes them easier to afford and reduces the need for a large loan. However, their reliability can vary. Some used cars are well-maintained and dependable, while others may require repairs sooner than expected.

Key Differences That Affect Your Decision

The difference between new and used cars mainly comes down to a few key factors that directly affect your cost, reliability, and long-term value.

- Upfront cost vs reliability: New cars require a higher upfront investment but offer more reliability and fewer unexpected problems. Used cars are more affordable but may come with some uncertainty in condition and future maintenance

- Value loss over time: New cars drop in value quickly in the first few years, which means you lose money early. Used cars have already gone through this steep decline, so their value remains more stable

- Ownership experience: New cars provide a more stable and low-risk experience, while used cars may require more attention and maintenance over time

Cost Difference Between New and Used Cars

Cost is often the biggest deciding factor because it affects both what you pay upfront and how manageable car ownership feels over time. Looking beyond the purchase price helps you understand what you can realistically afford.

Purchase Price Comparison

New cars come with a higher upfront price because you are paying for a vehicle with no prior use, full warranty coverage, and the latest features. This often means a larger down payment or higher monthly payments, which can put pressure on your finances if your budget is limited.

Used cars are more affordable because they have already gone through early depreciation. This lower entry cost makes it easier to buy without taking on a large loan. For many first-time buyers, this also creates more flexibility, allowing them to choose a better model or trim within the same budget.

Your monthly payment and loan terms also affect affordability over time, especially when you consider how car financing works.

Insurance and Running Costs

Auto insurance is typically higher for new cars due to their higher value and repair costs. This increases your monthly expenses even after you have purchased the car.

Used cars usually cost less to insure, which helps reduce ongoing expenses. However, maintenance is where the difference becomes more noticeable. New cars tend to have predictable service needs and fewer issues early on. Used cars may require replacements such as tires, brakes, or batteries sooner, depending on how they were used and maintained.

Total Cost Over Time

The total cost of owning a car includes depreciation, insurance, maintenance, and unexpected expenses over time.

New cars drop in value early in ownership. This means a portion of the money you spend is lost early, even if the car remains reliable. For buyers planning to upgrade in a few years, this can have a noticeable financial impact.

Used cars, on the other hand, have already gone through the steepest value drop. This helps you retain more of your money over time. However, they may come with unexpected repair costs, especially if the vehicle was not maintained properly by previous owners.

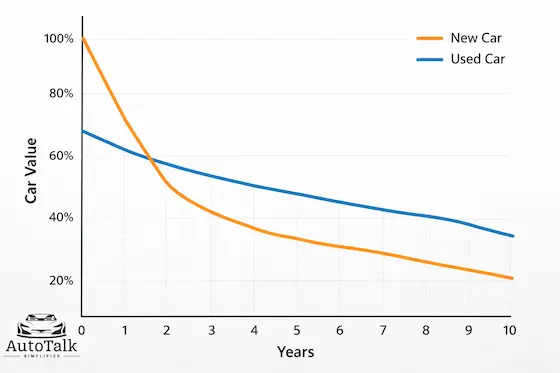

New vs Used Car Depreciation Explained

New cars lose value much faster than used cars, especially in the first few years, which means you lose more money early if you buy new. Used cars depreciate more slowly because most of the value drop has already happened, helping you retain more value over time.

Why New Cars Lose Value Faster

New cars experience the biggest drop in value during the first year of ownership. As soon as the car is driven off the lot, it is no longer considered new, and its market value decreases immediately.

This early depreciation happens because buyers are willing to pay more for a brand-new vehicle. Once that status is gone, the price adjusts quickly. Over the next few years, the value continues to drop at a steady rate.

For a first-time buyer, this means you are paying more upfront for something that will lose a significant portion of its value early. This matters most if you plan to sell or upgrade the car within a few years, as you may not recover much of what you paid.

Why Used Cars Depreciate Slower

Used cars depreciate at a slower rate because they have already gone through the steepest value loss. The previous owner has absorbed most of that initial drop.

This makes used cars more financially efficient in terms of value retention. You are buying the car closer to its actual market value rather than its original price.

For first-time buyers, this means you lose less money over time, especially if you plan to resell the car later. However, this benefit should be balanced with the possibility of higher maintenance or repair costs depending on the vehicle’s condition.

Pros and Cons of New Car vs Used Car

Choosing between a used car and a new car comes down to how much you want to spend and how much uncertainty you are willing to accept. A new car offers a more stable experience along with modern features, while a used car helps you save money but may require more attention over time.

Pros of Buying a New Car

New cars offer a more predictable and low-stress ownership experience, which is especially helpful for first-time buyers.

- Reliability: New cars are less likely to have issues in the early years, which means you can drive with more confidence and fewer interruptions

- Warranty coverage: Most repairs are covered by the manufacturer, so you are less likely to face unexpected expenses during the first few years

- Latest features: You get modern safety systems and updated technology, which can improve both convenience and overall driving safety

These benefits make new cars a good choice if you want peace of mind and a smoother ownership experience from day one.

Cons of Buying a New Car

The biggest downside of a new car is the higher cost and how quickly it loses value.

- Higher purchase price: You pay more upfront or take on larger monthly payments, which can limit your budget for other expenses.

- Early value drop: The car loses a significant portion of its value early. It means you may not recover much of what you paid if you sell it soon.

- Higher insurance costs: Insurance premiums are higher due to the car’s value, increasing your monthly ownership cost.

These factors make new cars less ideal if your goal is to keep overall costs low.

Pros of Buying a Used Car

Used cars are often the more practical option if your priority is affordability and long-term value.

- Lower purchase price: Easier to afford, which helps you avoid large loans and reduces financial pressure early on.

- Better value retention: The car holds its value better, so you lose less money over time compared to a new car.

- Lower insurance costs: Cheaper insurance helps keep your monthly expenses manageable.

These advantages make used cars a strong option if you want to balance cost and value.

Cons of Buying a Used Car

Used cars can come with some uncertainty, especially if their history is not fully known.

- Unknown condition: Past usage and maintenance affect reliability, which means you need to be more careful when choosing a vehicle

- Possible repair costs: You may need to replace parts sooner, leading to unexpected expenses after purchase

- Fewer modern features: Older models may lack newer safety or technology features, which can affect convenience and driving experience

These drawbacks mean a used car may require more effort and attention to maintain over time.

In simple terms, a new car reduces uncertainty, while a used car reduces cost.

How to Decide Between a New Car vs Used Car

If you are wondering should I buy a new or used car, the answer depends on how much you can spend, how long you plan to keep the car, and how comfortable you are handling maintenance and repairs. There is no one-size-fits-all choice, but a few clear factors can help you decide what fits your situation best.

When a New Car Makes Sense

A new car is a better choice if you want a more stable and low-maintenance ownership experience.

- Stable budget: You can comfortably afford higher monthly payments without stretching your finances

- Long-term ownership: You plan to keep the car for many years, which helps balance out the higher upfront cost

- Preference for reliability: You want fewer unexpected problems and a smoother ownership experience

In these situations, paying more upfront can make sense because it reduces stress and gives you more control over your ownership experience.

When a Used Car Is the Better Choice

A used car makes more sense if your priority is saving money and getting better value for your budget.

- Limited budget: You want to keep upfront costs low and avoid large loans or high monthly payments

- Short-term ownership: You may upgrade or change cars in a few years, so avoiding heavy depreciation matters more

- Value-focused mindset: You want to get the most value for your money, even if it means accepting some uncertainty

In these cases, a used car can help you stay financially comfortable while still meeting your basic needs.

Quick Decision Checklist

Use these points to decide which option fits your situation better:

- Can you comfortably afford higher monthly payments without financial stress?

- Do you plan to keep the car for many years?

- Are you comfortable handling possible repairs or maintenance issues?

- Do you prefer peace of mind or saving money upfront?

Frequently Asked Questions

Is it better to buy a new or used car for long-term ownership?

A new car is usually better for long-term ownership because it offers reliability and fewer repair issues in the early years. However, a well-maintained used car can still be a good long-term option if you want to save money upfront.

How many miles is too much for a used car?

There is no fixed number, but cars with over 100,000 miles may require more maintenance depending on how they were used and maintained. A well-maintained high-mileage car can still be reliable.

Do new cars really save money on maintenance?

Yes, new cars usually have lower maintenance costs in the first few years because they come with warranties and have less wear and tear. However, this advantage reduces over time.

Can a used car be as reliable as a new car?

A used car can be reliable if it has been properly maintained and inspected before purchase. However, it may still carry more risk compared to a new car.

Conclusion

Choosing between a new car vs used car comes down to what matters more to you: lower upfront cost or a more predictable ownership experience. New cars offer reliability, warranty coverage, and modern features, while used cars help you save money and retain more value over time.

There is no single right choice. The best option depends on your budget, how long you plan to keep the car, and how comfortable you are with possible risks. Focusing on these factors will help you make a confident and practical decision as a first-time buyer.