How car financing works is based on a simple idea: you borrow money to buy a car and repay it over time in monthly installments. If you are buying your first car, financing is one of the most important parts of the process. The financing choice you make affects your monthly payments, loan length, and total cost, which directly impacts your budget.

Many first-time buyers use financing because it makes car ownership more accessible. But without understanding how it works, it is easy to choose a plan that does not fit your financial situation.

Understanding financing is just one part of learning how to buy your first car. This guide focuses on financing so you can make clearer decisions when it comes to payments, options, and lender requirements.

What Is Car Financing?

Car financing is when a lender provides money to help you buy a car, and you repay it over time through fixed monthly payments. Instead of paying the full price upfront, first-time buyers can spread the cost across a set period. The total repayment usually includes the borrowed amount plus interest.

Paying Cash vs Financing

The main difference between paying cash and financing is how the cost of the car is paid. With cash, you pay the full price upfront and own the car immediately. There are no future payments.

However, with financing, the cost is divided into smaller payments over time. You repay the borrowed amount in installments, along with interest, based on agreed terms.

Whether you choose a new or used car, financing usually increases the total cost. However, not everyone can afford to pay the full amount upfront. Financing allows you to own a vehicle by spreading the cost into monthly payments that are easier to manage.

Who Is Involved in Car Financing

Car financing usually involves three main parties working together to complete the purchase and set up the repayment structure. Each plays a specific role in the process.

- You (the buyer): the person purchasing the vehicle and agreeing to repay the loan

- The lender: the bank, credit union, or financial institution that provides the money

- The dealership: the seller that completes the transaction and may help arrange financing

Basic Idea Behind Financing

There are different types of car financing, but they all follow the same basic idea. A lender pays for the vehicle upfront, and you repay that amount over time based on agreed terms such as loan length and payment schedule.

Understanding this structure helps you compare financing options more clearly and choose one that fits your financial situation.

Why Most Buyers Use Car Financing

Most buyers use car financing because it allows them to afford a vehicle without paying the full price upfront. Financing spreads the cost over time, making car ownership more accessible instead of requiring a large one-time payment.

It also allows buyers to start using a vehicle sooner while paying in fixed monthly installments. This flexibility is one of the main reasons financing is so common.

Ways to Finance a Car

There are several ways to finance a car, including loans, leasing, dealership financing, and bank or credit union financing. Each option differs in ownership, payment structure, and flexibility.

Car Loans

A car loan is the most common financing method used by buyers across America. You borrow money from a lender to purchase the vehicle and repay it over time through fixed monthly payments.

Once the loan is fully repaid, you own the car. This makes car loans a preferred option for buyers who want full ownership after completing their payments.

Leasing

Leasing allows you to use a car for a fixed period instead of owning it. You make monthly payments to drive the vehicle, but you do not build ownership during the lease term. This is the key difference when comparing a car loan vs car lease, since a loan leads to ownership while leasing focuses on usage.

Leasing often comes with lower monthly payments compared to loans. At the end of the lease, you can return the car or choose to buy it, depending on the agreement.

Dealership Financing

Dealership financing is arranged directly through the dealership where you buy the car. Dealers often work with multiple lenders to offer financing options in one place.

This option is convenient because it allows you to handle both the purchase and financing at the same time. Some dealerships may also offer promotional interest rates for qualified buyers.

Bank or Credit Union Financing

You can also arrange financing independently through a bank or credit union before visiting a dealership. This allows you to compare interest rates and loan terms in advance.

Getting pre-approved financing can give you a clearer idea of your budget and improve your confidence during the buying process.

Understanding the Financing Structure

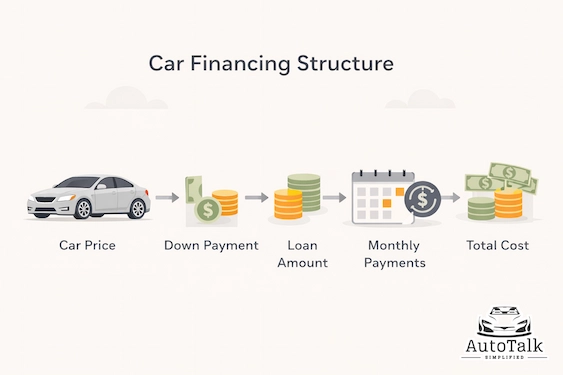

To understand how car financing works, you need to know how the cost is divided into key parts: down payment, monthly payments, and loan term. These elements determine how much you pay upfront, each month, and over time.

Down Payment

A car down payment is the amount you pay upfront when buying a vehicle. It reduces the total amount you need to borrow from the lender.

A higher down payment lowers your loan amount, which can reduce your monthly payments and the total interest you pay over time. It can also improve your chances of getting approved for financing.

Understanding how car down payments work helps you decide how much to pay upfront based on your budget and savings.

Monthly Payments

Monthly payments are the fixed amounts you pay regularly to repay your loan. These payments are based on the loan amount, interest rate, and loan term.

For example:

- Vehicle price: $30,000

- Down payment: $5,000

- Loan amount: $25,000

- Loan term: 60 months

In this case, your monthly payment is based on the $25,000 loan and the agreed interest rate. This is how monthly payments for car financing are structured.

Loan Term

The loan term is the length of time you take to repay the loan. It is usually measured in months, such as 36, 48, or 60 months.

A shorter loan term usually means higher monthly payments but lower total interest. A longer loan term reduces your monthly payments but increases the total interest you pay over time.

This is an important part of how car financing works, because the loan term directly affects both affordability and total cost.

How Car Financing Works

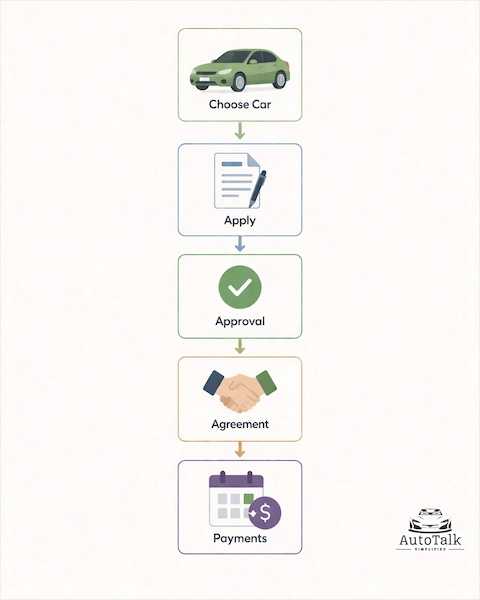

Understanding how car financing actually works is easier when you break it down into simple steps, from choosing a vehicle to setting up your monthly payments. For first-time buyers, the process may seem complex at first, but it follows a clear sequence.

Choose a Vehicle and Determine the Price

The process starts when you select a vehicle and agree on its price. This includes the cost of the car along with any additional fees such as taxes or registration.

The total price of the vehicle becomes the starting point for your financing.

Apply for Financing

Once you know the price, you apply for financing either through a dealership or directly with a lender such as a bank or credit union. At this stage, you provide basic financial information, including your income, employment details, and credit history.

Lender Reviews Your Application

The lender reviews your financial profile to decide whether to approve your application. They evaluate your ability to repay the loan based on your income, credit history, and existing financial obligations.

This step determines your approval status, interest rate, and loan terms.

Loan Approval and Agreement

If your application is approved, the lender offers a financing agreement. This includes details such as the loan amount, interest rate, monthly payment, and loan term. You review these terms and decide whether to accept the offer.

Payment Schedule Begins

Once you accept the agreement, the financing is finalized. The lender pays the dealership, and you begin making monthly payments to the lender according to the agreed schedule. These payments continue until the loan is fully repaid.

This entire step-by-step flow explains how car financing works in a practical way.

Requirements for Car Financing

The basic requirements for financing a car depend on your financial profile and ability to repay the loan. Lenders evaluate these key factors to decide approval and loan terms. Understanding these requirements helps you prepare in advance and improves your chances of getting better financing terms.

Credit Score

Your credit score is one of the most important factors in financing approval. It reflects your past borrowing behavior and how reliably you have repaid loans or credit.

A higher credit score for car financing usually leads to better interest rates and easier approval. A lower score may still qualify, but often with higher interest rates or stricter terms.

Income and Financial Stability

Lenders also evaluate your income and overall financial stability to ensure you can manage monthly payments.

They may look at your employment history, monthly income, and existing financial obligations. This helps them determine whether the loan fits within your financial capacity.

Identification and Documentation

To complete the application process, you need to provide certain documents that verify your identity and financial details. Please understand that paperwork required to purchase a car are entirely different from the car ownership documents.

This includes proof of identity, proof of income, and sometimes proof of residence. These documents help lenders confirm the information provided in your application and complete the approval process.

This is generally what is needed to finance a car, and having these documents ready can make the process smoother and faster.

Pros and Risks of Car Financing

Understanding how car financing works also means looking at both the benefits and the potential drawbacks. Financing can make buying a car easier, but it also comes with long-term responsibilities.

Benefits of Car Financing

Financing allows you to buy a car without waiting years to save the full amount. This makes vehicle ownership more accessible, especially when you need reliable transportation sooner.

It also spreads the cost over time, which helps you manage your budget through predictable monthly payments. In some cases, making timely payments can also help build your credit history.

Risks of Car Financing

Financing increases the total cost of the car because of interest. Even though monthly payments may feel manageable, you often pay more overall compared to paying in cash.

It also creates a long-term financial commitment. Missing payments can affect your credit and lead to additional charges.

Another risk is that the car may lose value faster than you repay the loan, which can leave you owing more than the vehicle is worth.

Financing Tips for First-Time Car Buyers

If you are financing a car for the first time, a few simple steps can help you make better decisions and avoid common mistakes.

Compare Financing Options

Do not choose the first financing offer you receive. Different lenders may offer different interest rates and loan terms. Comparing options helps you find a plan that fits your budget and reduces your total cost over time.

Check Your Credit Before Applying

Your credit profile plays an important role in financing approval and interest rates. Reviewing your credit in advance helps you understand what to expect. If needed, you can take steps to improve your credit before applying, which may help you secure better terms.

Plan for Total Ownership Costs

Financing is only one part of owning a car. You also need to budget for fuel, insurance, maintenance, and registration. Planning for these costs helps ensure your monthly payments remain manageable within your overall budget.

Understand Loan Terms Clearly

Before signing any agreement, take time to understand the loan details. This includes the interest rate, loan term, monthly payment, and total repayment amount. Clear understanding helps you avoid unexpected costs and choose a financing plan that matches your financial situation.

Frequently Asked Questions

What credit score is needed to finance a car?

There is no single credit score requirement for car financing, but lenders in the U.S. generally follow these ranges:

- Excellent: 750 and above

- Good: 700–749

- Fair/Average: 650–699

- Poor: below 650

Most lenders prefer a score of 660 or higher for better approval chances and lower interest rates. Lower scores may still qualify, but usually with higher interest rates and stricter terms.

How much down payment is required to finance a car?

There is no fixed amount required for a car down payment, but it is usually based on a percentage of the car’s price. In general, it is considered ideal to put down at least 10% to 20% of the vehicle’s value. This range helps reduce your loan amount while keeping your savings balanced.

A higher down payment lowers your monthly payments and reduces the total interest you pay. It can also improve your chances of getting approved for financing.

Is leasing considered financing?

Yes, leasing is considered a type of financing because you make monthly payments to use a vehicle over a fixed period. However, unlike loans, leasing does not lead to ownership unless you choose to buy the car at the end of the lease term.

How car financing affects monthly payments?

Car financing affects your monthly payments based on three main factors: loan amount, interest rate, and loan term. A higher loan amount or interest rate increases your monthly payment. A longer loan term lowers your monthly payment but increases the total interest you pay over time.

Understanding this balance helps you choose a payment that fits your budget without increasing your overall cost unnecessarily.

Can first-time buyers qualify for car financing?

Yes, first-time buyers can qualify for financing even without a long credit history. Lenders may look more closely at income and financial stability in such cases.

Preparing your documents and understanding what is needed to finance a car can improve your chances of approval.

Conclusion

Understanding how car financing works helps you make clearer and more confident car buying decisions.

Financing allows you to spread the cost over time, but it also affects your total expense and long-term commitment. Knowing how it is structured, what lenders look for, and how different options work helps you avoid common mistakes.

By comparing offers, reviewing your budget, and understanding the terms before committing, you can use financing in a way that fits your financial situation.

Confused about how car financing actually works?

Ask in the comments, and I’ll help you understand what generally matters and what to pay attention to when comparing financing options.